Introduction

The government has introduced strict rules to protect small businesses from delayed payments. Many MSMEs face problems when buyers do not pay on time. This affects their cash flow and business operations.

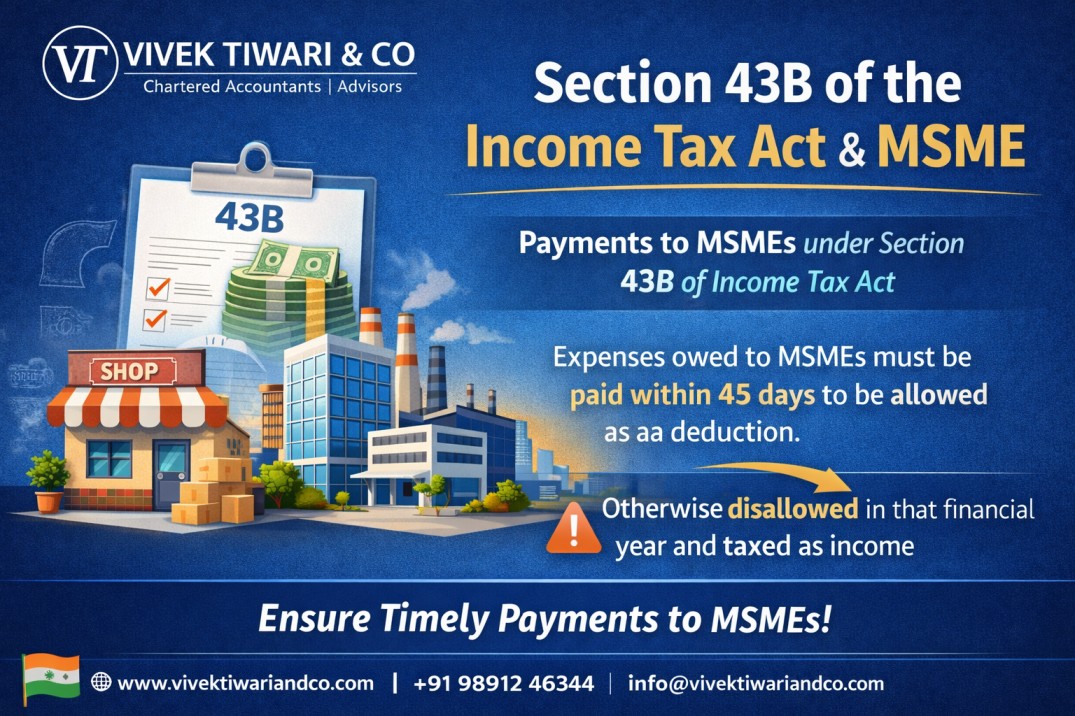

To solve this problem, a new rule was added under the income tax law called MSME Section 43B(h).

This rule is very important for both buyers and MSME classified businesses. It also affects income tax calculation.

In this guide, you will understand everything in simple words.

What is MSME Section 43B(h)?

MSME Section 43B(h) is a rule under the Income Tax Act that applies to payments made to MSME businesses.

According to this rule:

If a buyer does not pay an MSME supplier within the allowed time, the buyer cannot claim that expense as a tax deduction.

This means the buyer will have to pay more tax.

This rule encourages buyers to make payments on time.

Payment Time Limit Under This Rule

The payment time depends on the agreement between buyer and MSME.

If there is a written agreement:

- Payment must be made within 45 days

If there is no written agreement:

- Payment must be made within 15 days

If payment is delayed beyond this time, tax deduction is not allowed.

Why This Rule is Important for MSME

This rule gives strong protection to MSME businesses.

Benefits include:

• Helps MSMEs get payment faster

• Improves cash flow

• Reduces payment delays

• Protects small businesses

• Encourages fair business practices

This is a major relief for small businesses.

Impact on Buyers

This rule creates responsibility for buyers.

If buyers do not pay MSME on time:

- They cannot claim tax deduction

- Their taxable income increases

- They pay more tax

This increases their tax burden.

So buyers prefer to clear MSME payments quickly.

Example to Understand Easily

Suppose:

A company purchases goods from an MSME for ₹5,00,000, and as per the law, the payment must be made within 45 days. These rules apply only if the supplier qualifies under the MSME Turnover Limit, which defines whether a business is classified as Micro, Small, or Medium based on its annual turnover. But if the company does not pay within 45 days, it becomes liable to pay interest and the expense may also be disallowed under Section 43B of the Income Tax Act.

Result:

The company cannot claim ₹5,00,000 as an expense in that year.

They will have to pay extra tax.

Who is Covered Under This Rule?

This rule applies to:

- Businesses buying from MSME suppliers

- Companies purchasing goods or services from MSMEs

- All taxpayers who deal with MSME

MSMEs must be registered to get this benefit.

How MSME Registration Helps

MSME registration makes your business legally protected.

Benefits include:

- Protection under payment law

- Government scheme benefits

- Easy loan approval

- Business growth support

Without MSME registration, you cannot claim these benefits.

How Vivek Tiwari & Co Can Help You

Many business owners are confused about compliance.

Vivek Tiwari & Co helps with:

- MSME registration

- Income tax compliance

- Section 43B(h) guidance

- Documentation support

- Complete consultancy

Their experts make compliance easy.

Conclusion

MSME Section 43B(h) is an important rule to protect small businesses from delayed payments.

It also affects buyers’ tax deductions.

MSME registration and proper compliance are very important.

If you need help, Vivek Tiwari & Co can guide you professionally.

FAQ

What is MSME Section 43B(h)?

It is an income tax rule that disallows tax deduction if payment to MSME is not made on time.

What is the time limit for MSME payment?

15 days without agreement and 45 days with agreement.

Who does Section 43B(h) apply to?

It applies to buyers who purchase from MSME businesses.

Is MSME registration required?

Yes, MSME registration is required to get protection.